Income protection insurance is not a grudge purchase — it is the single most powerful wealth preservation tool most dual-income Australian households are dangerously underusing.

April is Financial Literacy Month in Australia — and this year, the theme that keeps surfacing in every serious wealth conversation is one that rarely gets the attention it deserves: protection. Not protection as fear. Not insurance as a monthly bill you resent paying. But insurance as a deliberate, strategic act of wealth preservation — the kind that keeps your financial plan intact when life decides to go sideways.

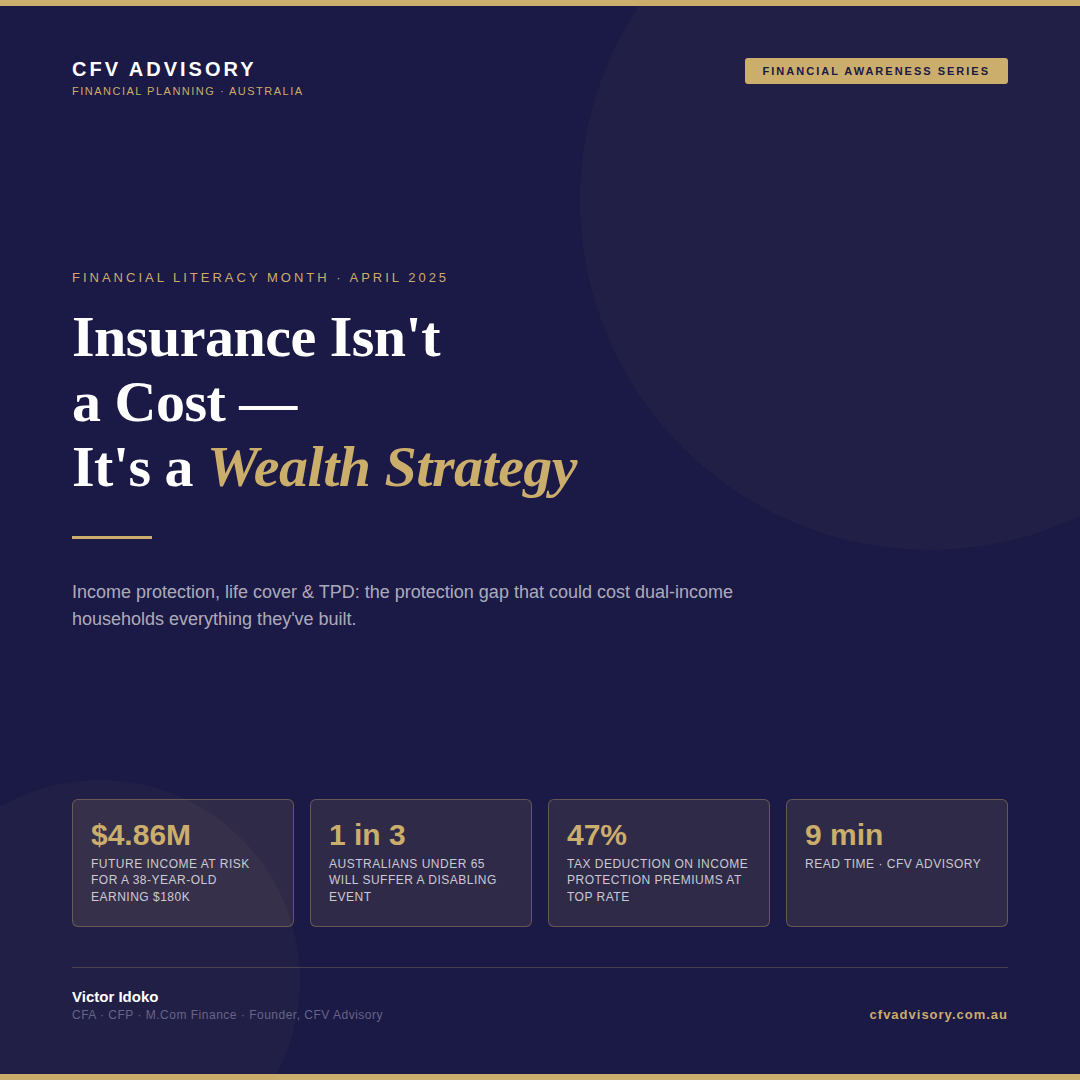

Consider this: a 38-year-old professional earning $180,000 per year has approximately 27 working years ahead. That is $4.86 million in future earnings — before investment returns, super growth, or salary increases. Yet the vast majority of dual-income households treat that income stream as an assumption rather than an asset to be protected. The result? When illness, injury, or death strikes — and statistically, for one in three Australians under 65, it will — the financial consequences cascade fast.

Financial stress doesn’t stay at home. Research consistently shows it follows people into the workplace — affecting productivity, decision-making, relationships, and long-term career trajectory. Insurance is what prevents a health event from becoming a wealth event. And in a high-income household where the lifestyle, the mortgage, the school fees, and the investment strategy are all built on two incomes — the cost of being uninsured is not the premium you save. It is everything you lose.

“A 38-year-old earning $180K has $4.86 million in future income ahead. That income stream is an asset. Most Australians treat it as a given — until the day it stops.”

— Victor Idoko, CFA · CFP · M.Com Finance | CFV Advisory

FINANCIAL AWARENESS SERIES

The Three Pillars of Personal Risk Protection

01

Income Protection

Replaces up to 70% of income if illness or injury prevents you from working. The foundation of any protection strategy.

02

Life Insurance

Pays a lump sum on death. Clears debts, funds dependants, and preserves the household wealth plan your family depends on.

03

TPD Cover

Lump sum if you become totally and permanently disabled. Often the most overlooked cover — and the most financially devastating gap.

The Real Cost of Being Uninsured in Australia

Most Australians significantly underestimate the financial cost of a prolonged absence from work. The headline figure — your monthly income — is only the beginning. Additionally, there are the super contributions that stop accumulating, the investment programme that gets paused, the mortgage offset that drains rather than grows, and the compounding opportunity cost that silently compounds year after year.

For a dual-income household earning $280,000 combined, a single income earner being out of work for 12 months means approximately $140,000 in lost income — before accounting for the additional medical costs, the lifestyle adjustments, and the wealth plan that quietly unravels in the background. Furthermore, superannuation contributions typically cease during an extended leave, removing the tax-effective compounding that makes up a significant portion of long-term retirement wealth.

The Australian Bureau of Statistics estimates that one in three people aged 34 to 65 will suffer a disability that sidelines them for more than three months. Yet most Australian households carry insurance that is woefully misaligned with their actual income, lifestyle, and financial obligations. Consequently, the protection gap in this country remains one of the most significant — and least discussed — risks to household wealth.

The time-cost compounds further when you consider what does not happen during an uninsured absence. For example, an investment property purchase planned for year three gets pushed to year five. A salary sacrifice strategy that was building meaningful super balances gets discontinued. A debt recycling programme — one of the most powerful tax-effective wealth tools available to Australian households — pauses entirely. As a result, the true cost of an uninsured period is not the missing income. It is the derailed trajectory.

⚠ KEY INSIGHT

For a $280K household, a 12-month disability event with no income protection cover can result in $140,000+ in lost income, $15,000–$25,000 in lost super accumulation, and a 2–5 year delay to every major wealth-building milestone on the plan.

Income Protection Insurance: What You’re Actually Buying

Income protection is precisely what the name suggests: a monthly benefit — typically up to 70% of your pre-disability income — paid while you are unable to work due to illness or injury. For high-income professionals, this is not a luxury. It is the structural foundation on which every other element of a financial plan depends.

There are two important variables that determine the quality of an income protection policy. First, the waiting period — the time between when you stop working and when payments begin. This is typically 30, 60, or 90 days. Shorter waiting periods mean higher premiums, but they also mean your emergency fund takes less of a hit. Second, the benefit period — how long the policy will pay. A two-year benefit period is materially less protective than a policy that pays to age 65. For a 35-year-old, a two-year policy has a 30-year blind spot.

Crucially, income protection premiums — when held outside superannuation — are generally tax-deductible under ATO rules. For someone in the 47% marginal tax bracket (income over $180,001), this means the government is effectively co-funding nearly half the premium. This changes the economics entirely — and transforms income protection from a grudge expense into one of the most tax-efficient purchases a high earner can make.

Moreover, the structure of the policy matters enormously. Agreed value policies — where the benefit amount is locked in at policy inception — provide greater certainty, particularly for professionals whose income fluctuates with bonuses or commissions. Indemnity policies, on the other hand, pay based on income at time of claim, which can create gaps if your earnings have grown since the policy was taken out.

💳 TAX ANGLE

For a professional earning $180,000, a $3,000/year income protection premium held outside super is effectively $1,590 after the ATO deduction at 47% marginal rate. That is $132.50 per month to protect a $15,000 monthly income. The risk-reward ratio is difficult to argue with.

Life Cover and TPD: The Overlooked Half of the Protection Equation

Life insurance and total and permanent disability (TPD) cover are often bundled with super — which creates a false sense of security. The reality is that default super-linked cover is typically calculated on a unit basis designed for the average Australian, not for a professional household with a $900,000 mortgage, two dependent children, and a wealth plan built on compound growth over the next two decades.

Life insurance should, at minimum, cover the following: outstanding debts (including the home loan), income replacement for the surviving partner over a defined period, and the future cost of dependants including education. For a dual-income couple in their late 30s with a $800,000 mortgage, the target life cover figure is typically $1.5 million to $2.5 million per person — significantly above what most super funds provide by default.

TPD is arguably the most neglected cover type in Australia — and statistically, one of the most consequential. A TPD event does not just remove your income. It increases your household costs: medical expenses, home modifications, carer support, and the loss of your productive capacity over what could be decades. Furthermore, unlike death, a TPD event means you are still present — with needs, with dependants, and with a life expectancy that could extend another 40 or 50 years.

Therefore, TPD cover should be sized not just to clear debt, but to fund ongoing income replacement and lifestyle costs for the long term. A lump sum of $1 million invested at 5% annual drawdown provides roughly $50,000 per year — far short of what most professionals need to maintain their lifestyle. Consequently, a common benchmark for TPD cover in a high-income household is 10 to 15 times annual income, adjusted for existing assets and super balances.

⚠ COVERAGE BENCHMARK

Life cover: outstanding debts + 10 years income replacement + education costs for dependants. TPD cover: 10–15x annual income, net of existing assets. Super default cover covers, on average, less than 20% of what a professional household actually needs.

Financial Stress and the Workplace: Why This Matters Beyond the Balance Sheet

Financial Literacy Month exists because financial stress is not a private problem. It is a professional one, a relational one, and increasingly, a systemic one. AMP’s Financial Wellness Report estimated that financial stress costs Australian businesses over $47 billion annually in lost productivity — a figure driven almost entirely by employees who are worried about money, not performing at capacity, and making risk-averse career decisions driven by fear rather than strategy.

High-income professionals are not immune. In fact, because their lifestyles, mortgages, and obligations typically scale with income, they are often more exposed to the financial consequences of an income disruption — not less. The month-to-month buffer that might exist for a simpler financial profile is often absent for a household with a $4,000/month mortgage, active investment commitments, and school fees on the way.

Additionally, financial insecurity affects decision-making in ways that are difficult to measure but easy to feel. The professional who can’t afford to leave a toxic role because they have no financial buffer. The couple who avoid starting an investment programme because they’re already worried about the mortgage. The executive who delays seeing a specialist because they’re calculating whether it’s affordable. Insurance removes these calculations. Moreover, it removes the underlying anxiety that drives them — and that, in itself, has measurable economic value.

Put simply: a household with proper protection in place makes better financial decisions. They take appropriate investment risk and pursue career opportunities with confidence—without letting fear, conscious or unconscious, dilute their wealth strategy. Protection, in this sense, is not just about what happens when things go wrong. It is about what becomes possible when you know you’re covered.

📈 THE BIGGER PICTURE

Financial stress costs Australian businesses $47B+ annually in lost productivity. For dual-income professionals, the financial consequences of an uninsured income disruption extend far beyond the event itself — reshaping careers, relationships, and long-term wealth trajectories.

How to Think About Insurance as a Wealth Tool, Not a Worry Tool

The reframe that matters most is this: insurance is not about what might go wrong. It is about protecting what you’ve built — and what you’re building. Every $500,000 in investment assets, every year of super contributions, every equity stake in a property represents accumulated effort and opportunity. Insurance is the mechanism that ensures a single adverse event cannot erase it.

Think of it in terms of the CFV wealth protection framework: your insurance programme should be sized to your current wealth, your outstanding obligations, and your future earning capacity — not to a generic benchmark. As your wealth grows, your insurance needs evolve. A 32-year-old just starting their investment journey has different needs from a 45-year-old with $800,000 in equity and a growing portfolio.

Specifically, here is how strategically structured insurance integrates with a broader wealth plan. Income protection underwrites the cash flow that funds everything else — mortgage repayments, super contributions, investment instalments. Life cover ensures dependants are not left managing debt on a single income. TPD cover funds the long-term income replacement that a lump sum from super alone cannot provide. Together, these three covers create a structure where an adverse event is genuinely manageable — rather than catastrophic.

Furthermore, the right time to review your insurance is not after a health scare. It is now — when you’re healthy, insurable, and in a position to negotiate appropriate terms. Premiums are set at policy inception based on your health at that time. Waiting means higher premiums, potential exclusions, and in some cases, declining insurability altogether. Financial leakage takes many forms — and inadequate insurance coverage is one of the most expensive forms of all.

Insurance Cover: What a Properly Structured Plan Protects

Income Protection

Up to 70% income replacement. Tax-deductible outside super. Protects cash flow, mortgage, investment programme, and super contributions from being disrupted by illness or injury.

Life Insurance

Lump sum on death. Clears mortgage, provides income replacement for surviving partner, funds dependants’ education. Benchmark: debts + 10 years income + future costs.

TPD Cover

Lump sum if permanently unable to work. Funds decades of income replacement, care costs, and lifestyle adjustments. Benchmark: 10–15x annual income net of assets.

The Hidden Benefit

Peace of mind that enables better decision-making, appropriate investment risk-taking, and career moves from a position of security rather than fear. Insurance protects the plan — not just the moment.

What to Do Before the End of This Financial Year

The end of June matters for insurance just as it does for tax — and that convergence is not a coincidence. Before 30 June, there are meaningful actions a dual-income household can take to both optimise their protection and reduce their tax bill simultaneously.

First, review your current cover levels against your actual income, debts, and lifestyle — not what you had three years ago. Second, consider whether your income protection is held inside or outside super, as the tax treatment differs significantly. Third, speak to a financial adviser who specialises in protection strategy, not just product placement — because the structure of your insurance is often as important as the quantum of cover. In particular, review the ATO’s rules on salary sacrificing and insurance within super — the interaction between the two can affect your contributions cap.

If you want to understand what financial leakage looks like across your household, a structured audit is the place to start. Insurance gaps are, consistently, one of the largest and most expensive leaks we find — because unlike a subscription or a poor spending habit, the cost of an insurance gap only becomes visible when it is already too late to fix it.

Protection is not the opposite of wealth. It is the foundation of it. For this Financial Literacy Month, the most financially literate thing you can do is not read another article about investing. It is to make sure the wealth you’re already building has the structural protection it deserves.

About the Author

Victor Idoko CFA · CFP · M.Com Finance

Victor is the founder of CFV Advisory and author of 7 Basic Wealth Strategies. He works with dual-income professional households across Australia, helping them close the gap between high income and genuine, durable wealth. His practice specialises in protection strategy, tax-effective investing, and the financial architecture that lets professionals build wealth without sacrificing lifestyle.

TAKE THE NEXT STEP

Is Your Income Actually Protected?

Most dual-income households carry significant insurance gaps — and don’t discover them until it’s too late. In one conversation, we can review your current cover, identify the gaps, and show you how a properly structured protection plan integrates with your broader wealth strategy.

Book Your Complimentary Introduction

No obligation. No jargon. Just clarity on where you stand.

General Advice Disclaimer: The information in this article is general in nature and does not constitute personal financial advice. It has been prepared without taking into account your individual objectives, financial situation, or needs. Before acting on any information, you should consider its appropriateness to your circumstances and seek advice from a licensed financial adviser. Victor Idoko (AR No. [insert]) is an Authorised Representative of [AFSL holder]. CFV Advisory is a registered business operating under Australian financial services laws. Past performance is not indicative of future results. Insurance needs vary significantly between individuals — always obtain a Statement of Advice before making insurance decisions.