By Victor Idoko, CFA, CFP, M.Com (Finance)

If you’re a dual-income professional couple in Australia in your 30s or 40s, there’s a specific kind of frustration you might recognise:

You earn good money.

You’re responsible.

You’re not reckless.

And yet… money still feels tight.

Not “we can’t pay bills” tight.

More like “how do we earn this much and still feel like we’re treading water?” tight.

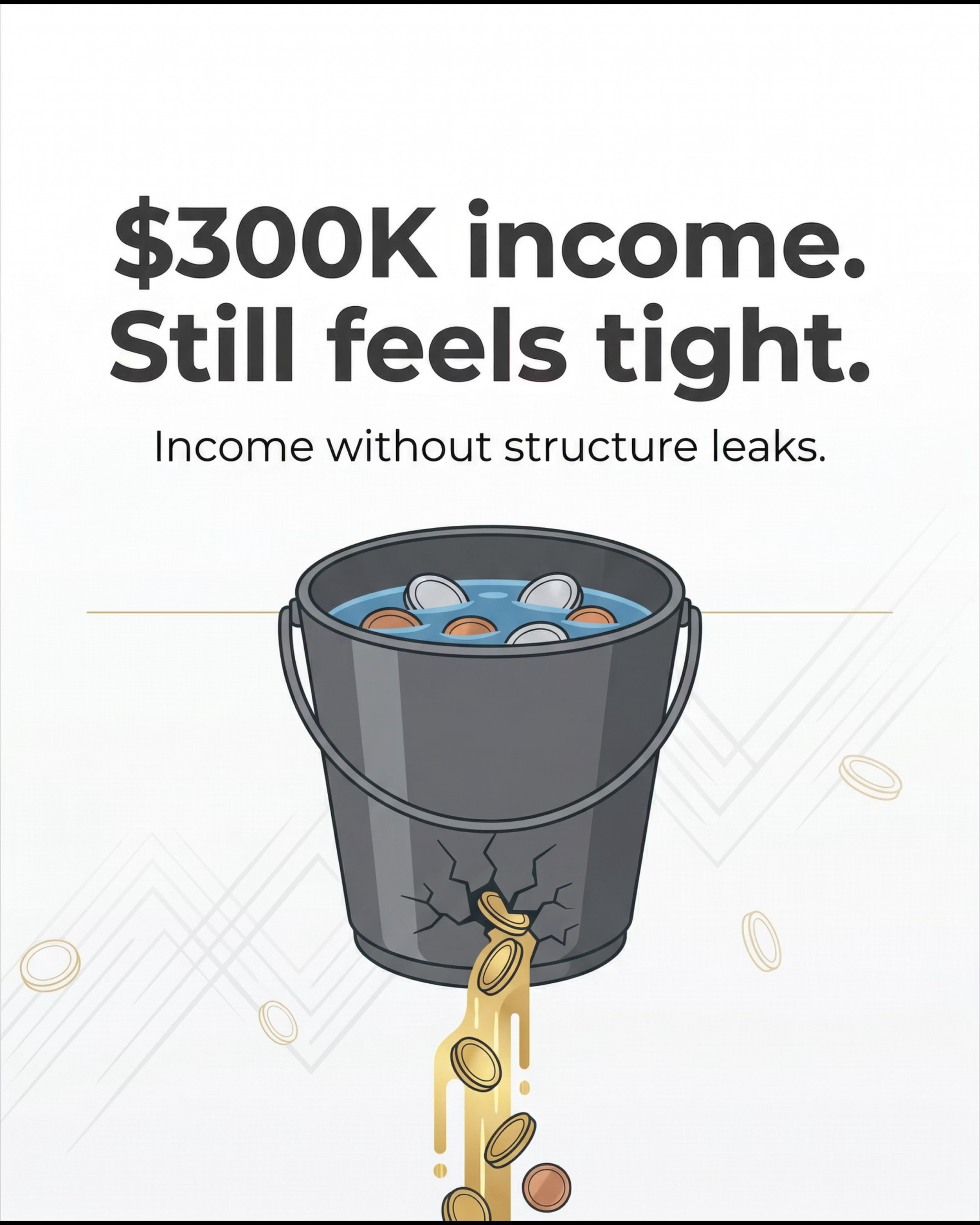

Here’s the proof that income alone doesn’t equal wealth:

I’ve sat with couples earning $300,000+ combined who genuinely couldn’t answer one basic question:

“Where does your money go each month?”

Not because they were lying.

Because their money was moving through a life with no system.

Income without systems leaks.

That’s the real problem.

The cash flow myth that traps high earners

Most people believe:

“If we just earn more, this will feel easier.”

Sometimes that’s true early on.

But past a certain point, higher income simply creates a new issue:

more money moving through an unstructured life.

When there’s no structure, high income doesn’t create peace. It creates:

- bigger defaults

- more convenience spending

- higher lifestyle standards

- and silent drift that’s hard to see until years pass

In other words: you don’t notice the leak because the boat is still floating.

Until you try to do something meaningful—invest consistently, pay down debt faster, build real buffers—and realise there isn’t as much spare as you expected.

Why money feels tight on $200K+ in Australia

Yes, the mortgage matters. Childcare matters. Cost of living matters.

But when I work with professional households in their 30s and 40s, the root cause is often more behavioural and structural than people expect.

1) Lifestyle creep isn’t splurging — it’s “standards”

Most high earners don’t blow money on one ridiculous thing.

The leak usually looks like:

- delivery food because everyone’s exhausted

- upgrades because “we’ve earned it”

- convenience because time is scarce

- subscriptions that feel small

- the “nice” version of everything becoming normal

None of it feels irresponsible.

It just quietly becomes the default.

2) Too many goals, no goal order

High-performing couples often try to fund everything at once:

- renovate

- travel

- pay down the mortgage

- invest

- private school planning

- help family

- upgrade cars

- build retirement

All valid goals.

But without a clear priority order, what happens is predictable:

- investing starts and stops

- buffers get raided

- the mortgage barely moves

- and you feel tight forever, even on a strong income

3) Your “system” is one account and vibes

Many households still run cash flow like this:

- salaries land in one account

- bills come out whenever

- savings happens “if there’s leftover”

- investing happens when someone remembers

- the offset gets dipped into

- credit cards bridge the gap

That isn’t a wealth system.

That’s improvisation.

And improvisation gets expensive when life gets busy.

4) You measure success by income, not progress

Income is what you earn.

Wealth is what you keep—and what you build consistently.

A household on $180K with strong structure can create more wealth than a household on $300K without it.

Because the second household has a bigger leak.

A real scenario (relatable to Australian professional couples)

A couple in their late 30s:

- both professionals

- combined income well above $200K

- a mortgage on a home they love

- kids in school / childcare

- super growing quietly in the background

They assumed their mortgage was the problem.

But once we looked closely, the real issue was simpler:

They had no cash-flow rules and no automation.

So every month became a new negotiation.

- “Are we okay?”

- “Can we afford this?”

- “Should we invest this month?”

- “Let’s start next month…”

And next month always arrived with another cost.

They weren’t failing financially.

They were operating without a system.

The Foundations fix: how high-income households stop the leak

This is where generational wealth actually starts—at the Foundations layer.

Not with a hot investment tip.

Not with a fancy product.

With a structure that makes progress inevitable.

1) Install a spending plan (without budget shame)

You don’t need to track every transaction.

You need rules.

At a minimum, your money needs to be split into:

- household operations (bills + living)

- wealth building (buffers + investing + debt reduction)

- guilt-free lifestyle (pre-approved spending)

When the rules are clear, decisions become calm.

2) Automate the plan on payday

Wealth builders don’t “save what’s left.”

They pay the plan first.

Automation removes:

- mood

- forgetfulness

- and negotiation

Bills happen automatically.

Buffers build automatically.

Investing happens automatically.

This is the difference between “we mean to” and “it happens.”

3) Create a buffer policy (not just a savings account)

Most families “have savings”… until it gets used for everything.

A buffer needs rules:

- what it’s for (true surprises)

- what it’s not for (lifestyle creep)

- how it gets replenished

- where it lives so it isn’t constantly raided

A buffer turns shocks into inconveniences instead of setbacks.

4) Decide goal order (this is the game changer)

If you want money to stop feeling tight, you need to stop funding ten goals at once.

Choose the order.

Fund in order.

Ignore the rest until the earlier goals are stable.

This is what creates momentum.

Because once priorities are clear, your income finally starts behaving like a tool—not a treadmill.

The real takeaway for high-income households

If you earn $200K–$300K+ and money still feels tight, don’t assume you’re bad with money.

Assume your system is incomplete.

Income isn’t the solution. Structure is.

Once Foundations are installed, three things happen:

- your household becomes calmer

- investing becomes consistent

- and wealth starts compounding quietly in the background

That’s the start of generational wealth: not a big moment, but a reliable system.

Call to action: book a consult

If you’re a dual-income professional household in your 30s or 40s and you want a clear cash-flow structure—so you can build wealth without feeling tight—book a consult.

About the author

Victor Idoko, CFA, CFP, M.Com (Finance) is the founder of CFV Advisory in Australia and Author of 7 Basic Wealth Strategies. With 11 years’ experience in financial planning, Victor is known for helping wealth builders and families create clear, practical structures to build, protect, and transfer wealth—without sacrificing lifestyle or relationships.

Victor holds globally recognised designations including the Chartered Financial Analyst (CFA) and Certified Financial Planner (CFP), alongside a Master of Commerce (Finance). His approach blends technical depth (strategy, tax-aware structuring, super and retirement planning, investment design) with the real-world family side of wealth—so plans don’t just look good on paper, they work in life.

If you want help applying this to your family, follow and read the next few series and book a meeting with Victor.

Any discussion in this article does not take into account your objectives, financial situation or needs. Before acting on it, you should consider whether it’s appropriate to you, in light of your objectives, financial situation or needs.